The Savings section of the Profile is where you will enter prospective annual contributions to a client's various investments. This includes contributions to 401(k) and IRAs, taxable brokerage accounts, Roth accounts, 529s, and much more.

There will be a handful of savings cards pre-populated within this section when you create a new client plan. You will always find one 401(k) savings card for each client. You may also see a Taxable savings card, depending on your plan settings.

For clients with 401(k) accounts, you can use the pre-populated 401(k) savings cards for one or both clients. Click on this card to open a data entry drawer on the right side of your screen, allowing you to input the details:

1

The Saving name will default to [Client's] 401(k), but you can enter a custom name if you'd like. In joint plans, you will also want to choose either the client or the co-client as the Owner.

2

Enter the client's annual Contribution to their 401(k). Depending on the option you choose in the Target field, this can be an annual dollar amount, a % of the client's income, or the maximum contribution amount.

3

Specify the duration of the contributions using the Saving starts and Saving ends fields. By default, these will be set to 'Already started' and '[Client's] retirement' respectively.

4

Enter the details of the employer match, starting with the Primary match (full or partial) and the Primary match to (% of client's contribution). If necessary, you can also specify the Secondary match and Secondary match to percentages.

A common example might look like a full match of 100% up to 3% of the client's contribution, and a partial match of 50% up to 5% of the client's contribution:

5

For non-elective employer matches, you can skip the primary and secondary matches and instead enter a Flat percent match or a Flat dollar match. These will occur regardless of employee contributions.

6

If some or all of the employer match is designated as a Roth contribution (as per Secure Act 2.0), indicate this percentage in the % of match to Roth field.

What does "Self-employed" do?

Checking the Self-employed box will cause this card to calculate employee/employer contributions based on the client's Self-employment income, rather than Salary income.

Please click on the dropdown arrows below for more information on...

Total employee contributions will be capped at the IRS maximum value ($23,500 for 2025, plus $7,500 catch-up at 50, $11,250 from 60-63). For salaried clients, 401(k) contributions will be deducted from the client's wages on Line 1 of the 1040. With the 'Self-employed' box checked, contributions will be treated as Adjustments to Income (Line 16 of Schedule 1, Line 10 of the 1040).

Sample tax forms can be viewed in the Tax > Tax Estimate > Details tab:

Client contributions can be tracked in two locations within the Retirement > Cash Flows:

The Summary tab > Planned Savings column

The Invested Asset tab > Planned Savings column

Employer matches can be found in the Invested Asset tab > Employer Match & Other column:

For clients that are not making 401(k) contributions, these cards can be removed. Hover your mouse over the card, click the 'x' icon that appears in the upper right, and then click Delete. If you remove a 401(k) card and need to add it back at any time, you can do so by clicking Add Saving > 401(k)/403(b)/457(b) > 401(k):

If your Planning Method setting is set to 'Modified Cash Flow Based' or 'Goal Based' as a default, a Taxable savings card will also be pre-populated in the Savings area. Use this card to reflect after-tax contributions into a taxable investment / brokerage account:

Start by choosing the client, co-client or joint as the Owner. Depending on your chosen Target option, enter the Contribution as an annual dollar amount or as a percentage of income. Lastly, dial in the Saving starts and Saving ends dates to determine the duration of the contributions.

If you have 'Annual dollar amount' chosen as your target you can enter an optional Annual Increase, which will be applied to the contribution amount each year within the cash flow projections.

Don't see a Taxable savings option?

If you are using a 'Cash Flow Based' planning method, any and all excess cash flows will be automatically saved and reinvested into the client's taxable account bucket. This function eliminates the need for you to manually enter taxable savings.

To learn more about the planning method setting and its impact on your client plans, feel free to reference the article below:

Taxable savings can be easily tracked within the Cash Flows module in the Retirement section. Within the Cash Flows > Summary, taxable savings will be reflected in the Net Flows column to the far right. Negative numbers in this column (numbers within parenthesis) indicate cash flow shortfalls. Excess income that is not being saved into the taxable bucket will be displayed in the 'Spend Unsaved Cash Flows' column:

Important Note on Taxable Savings:

Please note that taxable savings will only occur in years that clients have adequate income to make those savings. For example, if you enter $10,000 in taxable savings and the clients only have a $5,000 cash flow surplus in a given year, only $5,000 will be saved. In years with cash flow deficits, taxable savings will not occur.

To add additional savings to a client plan, click the blue 'Add Saving' button in the upper right. This will allow you to choose from a long list of savings options:

Below you will find a brief overview of each savings type, followed by additional information on data entry, taxation, and cash flow location. Remember that if you ever have any questions while entering client data, you can always reach out to the RightCapital Support Team for assistance!

Use these savings cards to reflect employee and employer contributions into employer-sponsored retirement plans (such as 401(k), 403(b), 457(b), and their Roth equivalents). Contributions to employer-sponsored plans will always occur within the cash flow projections, even in years with cash flow deficits.

Total contributions to all defined contribution plans (employee plus employer) will be capped at the IRS maximum value ($70,000 for 2025, plus $7,500 catch-up at 50, $11,250 from 60-63). You can track client savings and employer matches within the Cash Flows > Invested Asset tab.

Click on the dropdown arrows below for more details on data entry, contribution limits, and tax implications:

Data entry for these savings cards is identical to the process described above for 401(k) savings cards.

Total employee contributions across these accounts will be capped at the IRS maximum value ($23,500 for 2025, plus $7,500 catch-up at 50, $11,250 from 60-63).

For salaried clients, traditional 401(k) and 403(b) contributions are treated as W2 deductions and will reduce the client's income on Line 1 of the sample 1040 tax form. With the 'Self-employed' box checked, contributions will be treated as Adjustments to Income (Line 16 of the Schedule 1, Line 10 of the 1040).

Data entry for these savings cards is identical to the process described above for 401(k) savings cards.

Total employee and employer contributions across these accounts will be capped at the IRS maximum value ($23,500 for 2025, plus $7,500 catch-up at 50, $11,250 from 60-63).

For salaried clients, traditional 457(b) contributions are treated as W2 deductions and will reduce the client's income on Line 1 of the sample 1040 tax form. With the 'Self-employed' box checked, contributions will be treated as Adjustments to Income (Line 16 of the Schedule 1, Line 10 of the 1040).

Data entry for these savings cards is identical to the process described above for 401(k) savings cards.

For salaried clients, the employee contribution will be limited to a maximum of $23,500 for 2025, plus $7,500 catch-up at 50, $11,250 from 60-63. Solo 401(k) contributions will be deducted from the client's wages on Line 1 of the Sample 1040 Tax Form.

With the 'Self-employed' box checked, the maximum employee contribution will be $23,500 for 2025, plus 18.47% of the client's self-employment income (plus $7,500 catch-up at 50, $11,250 from 60-63). Solo 401(k) contributions will be treated as Adjustments to Income (Line 16 of the Schedule 1, Line 10 of the 1040).

Data entry for 401(a) savings cards is identical to the process described above for 401(k) savings cards, less the "% of match to Roth" option.

401(a) contributions will be capped at an employee + employer maximum of $70,000 for 2025.

For salaried clients, employee contributions will be deducted from the client's wages on Line 1 of the 1040. With the 'Self-employed' box checked, employee contributions will be treated as Adjustments to Income (Line 16 of the Schedule 1, Line 10 of the 1040).

Traditional, SEP and SIMPLE IRA contributions can be reflected via these savings cards. By default, IRA contributions will be funded using taxable assets in years with inadequate cash inflows.

IRA savings can be tracked within the Cash Flows > Summary > Planned Savings column, or within the Cash Flows > Invested Asset tab. Click on the dropdown arrows below for more details on data entry, contribution limits, and tax implications:

Data entry for these savings cards is identical to the process described above for 401(k) savings cards, less the employer match portion.

Contributions are capped at the IRS limit ($7,000 for 2025, plus $1,000 catch-up at 50). This cap includes both Traditional IRA and Roth IRA contributions.

Contributions less than the income limit will be considered tax deductible (Line 20 of the Schedule 1, Line 10 of the Sample 1040 Tax Form). In 2025, deductibility phases out between $79,000 and $89,000 of AGI for single; between $126,000 and $146,000 for joint. Over those thresholds, the total contribution will be considered nondeductible.

Data entry for these savings cards is identical to the process described above for 401(k) savings cards, less the employer match portion.

For salaried clients, all contributions are employer contributions. The contribution will be capped at the lesser of 25% of the client's salary, or the IRS maximum ($70,000 for 2025).

With the 'Self-employed' box checked, all contributions are employee contributions. The contribution will be capped at 18.47% of the client's self-employment income (with a maximum income limit of $350,000 for 2025). SEP IRA contributions will be treated as Adjustments to Income (Line 16 of the Schedule 1, Line 10 of the 1040).

Like other employer-sponsored plans, contributions to SEP plans will always occur within the cash flow projections, even in years with cash flow deficits.

Data entry for these savings cards is identical to the process described above for 401(k) savings cards, less the 'Flat dollar match' field.

Total employee contributions will be capped at the IRS maximum ($16,500 for 2025, plus $3,500 catch-up at 50, $5,250 from 60-63).

For salaried clients, contributions will be deducted from the client's wages on Line 1 of the 1040. With the 'Self-employed' box checked, contributions will be treated as Adjustments to Income (Line 16 of the Schedule 1, Line 10 of the 1040).

Like other employer-sponsored plans, contributions to SIMPLE plans will always occur within the cash flow projections, even in years with cash flow deficits.

Roth IRA contributions (including SEP and SIMPLE) can be reflected via these savings cards. There is an additional Backdoor Roth IRA savings card that reflects nondeductible IRA contributions that are then converted to a Roth IRA.

By default, Roth IRA contributions will be funded using taxable assets in years with inadequate cash inflows. If the "Use taxable account to fund IRA and 529 saving when current year cash flow is inadequate" setting is unchecked, Roth IRA contributions will not occur in years with cash flow deficits. You can find this setting in the Gear Icon > Settings > Methodology tab of each client plan.

Roth IRA savings can be tracked within the Cash Flows > Summary > Planned Savings column, or within the Cash Flows > Invested Asset tab. Click on the dropdown arrows below for more details on data entry, contribution limits, and income phase outs:

Data entry for these savings cards is identical to the process described above for 401(k) savings cards, less the employer match portion.

Contributions are capped at the IRS limit ($7,000 for 2025 + $1,000 catch-up for those 50 and over). This cap includes both Traditional IRA and Roth IRA contributions.

In 2025, contribution eligibility phases out between $150,000 and $165,000 of MAGI for single, and between $236,000 and $246,000 for joint. For married filing separately, the contribution phase out begins at $0 and ends at $10,000.

Data entry for these savings cards is identical to the process described above for 401(k) savings cards, less the employer match portion.

Contributions are capped at the IRS limit ($7,000 for 2025 + $1,000 catch-up for those 50 and over). This cap includes both Traditional IRA and Roth IRA contributions.

Backdoor savings cards reflect a nondeductible contribution to a traditional IRA that is then converted to a Roth IRA. This allows you to illustrate Roth IRA savings even if the client is over the Roth IRA contribution phase out.

Data entry for these savings cards is identical to the process described above for 401(k) savings cards, less the employer match portion.

For salaried clients, all contributions are employer contributions. The contribution will be capped at the lesser of 25% of the client's salary, or the IRS maximum ($70,000 for 2025).

With the 'Self-employed' box checked, all contributions are employee contributions. The contribution will be capped at 18.47% of the client's self-employment income (with a maximum income limit of $350,000 for 2025).

Like other employer-sponsored plans, contributions to SEP plans will always occur within the cash flow projections, even in years with cash flow deficits.

Data entry for these savings cards is identical to the process described above for 401(k) savings cards, less the 'Flat dollar match' field.

Total employee contributions will be capped at the IRS maximum ($16,500 for 2025, plus $3,500 catch-up at 50, $5,250 from 60-63).

Like other employer-sponsored plans, contributions to SIMPLE plans will always occur within the cash flow projections, even in years with cash flow deficits.

HSA savings cards are used to reflect both employee and employer contributions into a client's Health Savings Account. HSA contributions are pre-tax and will always occur within the cash flow projections, even in years with cash flow deficits.

Click on the dropdown arrows below for more details on:

Start by choosing the client or co-client as the Owner. Depending on your chosen Target option, enter the client's Contribution as an annual dollar amount, percentage of income, or the maximum contribution. Lastly, dial in the Saving starts and Saving ends dates to determine the duration of the contributions.

If you have 'Annual dollar amount' chosen as your target you can enter an optional Annual Increase, which will be applied to the contribution amount each year within the cash flow projections. The Flat dollar match field can be used to reflect an employer match.

Employee contributions are capped at the IRS limits for a single individual ($4,300 for 2025, plus $1,000 catch-up for age 55+) and for a family ($8,550 for 2025, plus $1,000 catch-up for age 55+).

Employee contributions are pre-tax and are treated as Adjustments to Income (Line 13 of the Schedule 1, Line 10 of the 1040) for tax purposes, reducing a client's AGI.

Client contributions can be tracked in two locations within the Retirement > Cash Flows:

The Summary tab > Planned Savings column

The Invested Asset tab > Planned Savings column

Employer matches can be found in the Invested Asset tab > Employer Match & Other column.

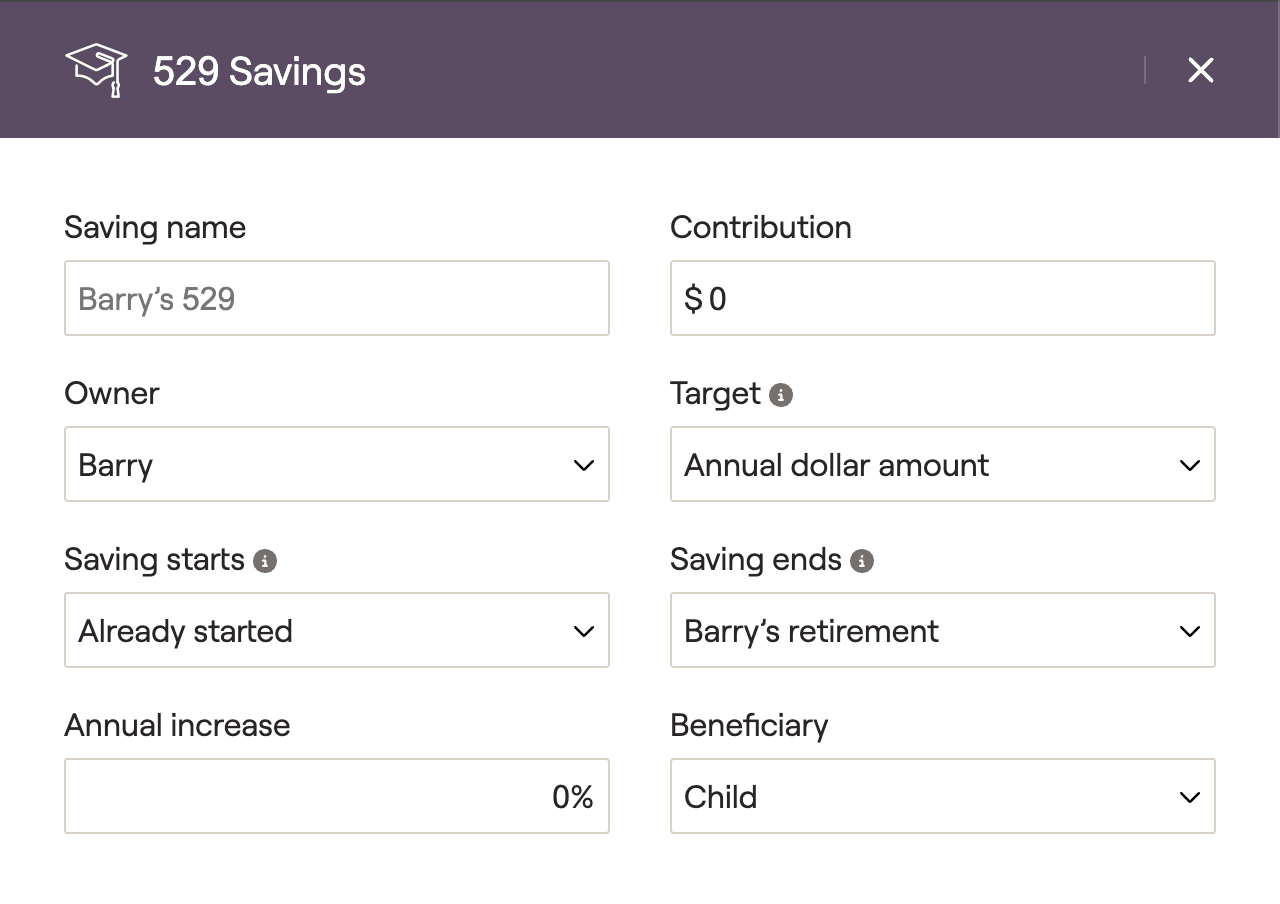

529 savings cards allow you to reflect contributions from the clients themselves, or from an individual outside of the plan. Please note that this card should also be used for UTMA, UGMA, and Coverdell ESA contributions, as all education savings accounts are lumped into the 529 account bucket in RightCapital.

Click on the dropdown arrows below for more details on:

Start by choosing either a client or outside individual as the Owner. Depending on your chosen Target option, enter the client's Contribution as an annual dollar amount or percentage of income. Lastly, dial in the Saving starts and Saving ends dates to determine the duration of the contributions. If you have 'Annual dollar amount' chosen as your target you can enter an optional Annual Increase.

The Beneficiary field can be used to assign a specific individual within the plan as the 529 beneficiary. If assigned to an individual, the 529 can be used to illustrate college funding for that student within the Education module. If set to 'Unassigned', the 529 savings will be used for all education goals regardless of the student.

There are no limits in the system on contributions to 529 plans. 529 savings are after-tax and are not deductible.

Client contributions can be tracked in two locations within the Retirement > Cash Flows:

The Summary tab > Planned Savings column

The Invested Asset tab > Planned Savings column

Outside contributions can be found in the Invested Asset tab > Employer Match & Other column.

By default, 529 contributions will be funded using taxable assets in years with inadequate cash inflows. If the "Use taxable account to fund IRA and 529 saving when current year cash flow is inadequate" setting is unchecked, 529 contributions will not occur in years with cash flow deficits. You can find this setting in the Gear Icon > Settings > Methodology tab of each client plan.

Allows you to reflect outside contributions to the Qualified Pension account bucket. These savings will be shown as an employer contribution, and can be tracked within the Retirement > Cash Flows > Invested Asset tab.

If the 'Self-employed' box is checked, the contribution will reflect as a client contribution, reducing the client's cash flows (Cash Flows > Summary > Planned Savings). Contributions will occur regardless of cash flow deficits, and will be treated as Adjustments to Income (Line 16 of the Schedule 1, Line 10 of the 1040).

Deferred Compensation

Allows you to reflect employee or employer contributions to the Non-Qualified Pension account bucket. Client contributions are pre-tax, and will occur each year regardless of cash flows deficits. These contributions will be deducted from the client's wages on Line 1 of the 1040. Both employee & employer contributions can be tracked in the Retirement > Cash Flows > Invested Asset tab.

Profit-Sharing

Allows you to reflect contributions to a profit-sharing plan, which will be added to the 401(k)/403(b) account bucket. For salaried clients, all contributions are employer contributions. The contribution will be capped at the lesser of 25% of the client's salary, or the IRS maximum ($70,000 for 2025, plus $7,500 catch-up at 50, $11,250 from 60-63).

With the 'Self-employed' box checked, all contributions are employee contributions. The contribution will be capped at 18.47% of the client's self-employment income, and contributions will be treated as Adjustments to Income (Line 16 of the Schedule 1, Line 10 of the 1040).

Employee Stock Purchase Plan (ESPP)

Allows you to reflect the purchase of shares in an ESPP. If the ESPP allows for the purchase of shares at a discount, you can enter the percentage discount as part of the savings card. ESPP savings will flow through to the Taxable account bucket. You will see the value reflected in the Retirement > Cash Flows > Summary > Net Flows column, just like Taxable savings. The incremental value provided by the discount will be shown as an employer contribution, which can be tracked in the Cash Flows > Invested Asset tab. ESPP contributions will be taxed like any other taxable assets; we do not factor in short-term capital gain rates for withdrawals within a year.

Employee Stock Ownership Plan (ESOP)

Allows you to reflect contributions to an ESOP, which will be added to the 401(k)/403(b) account bucket. For salaried clients, all contributions are employer contributions. The contribution will be capped at the lesser of 25% of the client's salary, or the IRS maximum ($70,000 for 2025, plus $7,500 catch-up at 50, $11,250 from 60-63).

With the 'Self-employed' box checked, all contributions are employee contributions. The contribution will be capped at 18.47% of the client's self-employment income, and contributions will be treated as Adjustments to Income (Line 16 of the Schedule 1, Line 10 of the 1040).

Bank

Allows you to model cash savings into the client's bank accounts / cash reserve. These funds will grow at the rate of return associated with your return assumption for Cash. Like taxable savings, bank savings will only occur in years that clients have adequate income inflows. Bank savings can be tracked within the Retirement > Cash Flows > Summary > Net Flows column.

The Bank savings card will only be visible if your Planning Method settingis set to 'Modified Cash Flow Based', and your Cash Management Method setting is set to one of the 'Treat Bank Acct as Cash' options.

Tax-Deferred

This card can be used to reflect outside contributions to a tax-deferred account. Anything entered as part of a Tax-Deferred savings card will be shown as an employer contribution, and be tracked in the Retirement > Cash Flows > Invested Asset tab. These cards are not subject to contribution limits.

There will be an additional variable in each card that allows you to select which account bucket the savings will flow to. The options for tax-deferred savings are:

401(k), 403(b), or other retirement plan

Traditional IRA or other IRA

Tax-Free

This card can be used to reflect outside contributions to a tax-free account. Anything entered as part of a Tax-Free savings card will be shown as an employer contribution, and be tracked in the Retirement > Cash Flows > Invested Asset tab.

There will be an additional variable in each card that allows you to select which account bucket the savings will flow to. The options for tax-free savings are:

Below is a table that illustrates which savings are funded from the client's income, and which savings are funded by the employer / from outside the plan. It also lists where employee and employer contributions can be found in the Retirement > Cash Flows > Accounts tab. Retirement savings will be capped at the IRS contribution limits, which increase by your tax inflation assumption as they are projected into the future.

*The value provided by the discount is reflected as an employer match

Employee Stock Ownership Plan

Employee (Self-Employment) / Employer (Salary)

401k/403b

401k/403b

Tax-Deferred

Outside Contribution

401k/403b or Traditional IRA

Tax-Free

Outside Contribution

Roth 401k/403b or Roth IRA

Employer Match Maximum

The maximum % match that can be entered into a savings card is 200%. If an employer match exceeds 200%, we recommend inputting that amount as a "flat dollar amount" match instead.

Contact Us

For additional assistance within RightCapital please contact our Support team.

Educational Webinars

RightCapital is committed to enabling your success. Each week, we cover essential planning modules and product updates.

RightCapital in Action

Check out our YouTube channel where we highlight Advisor Success Stories and share more Tips & Tricks!