The Goals section of the Profile is where you will identify and enter a client's goals into their financial plan. This includes retirement ages, retirement living expenses, and retirement health care & long-term care costs. It can also include any number of additional goals, such as college goals, travel goals, primary home relocations, asset purchases, and much more.

RightCapital will pre-populate a number of cards in this step of the data entry when you create a new client plan. Start by entering the retirement age(s), the retirement living expenses, and assumed health care and long-term care costs:

This will be the first card pre-populated in this area. Click on this card to specify the client and co-client's retirement ages:

The retirement ages you enter for each client will influence any other data entry cards that are set to start or end at the client's retirement. It will also determine when pre-retirement living expenses will stop, and retirement living expenses will begin. You can control whether retirement expenses begin at first or second retirement in the plan settings.

By default, RightCapital assumes the clients retire at the start of the year. Check the box to indicate a specific month of retirement for each client.

If you specify a calendar month, the age entered will determine the calendar year of retirement, and the month selected will indicate which month in that year they expect to retire. Please note that this may be before or after their birthday when they turn retirement age.

The Retirement Expense card can be utilized to capture the household's monthly retirement expenses within the projections.

Important Note on Living Expenses

When entering living expenses, please be mindful that this number should not include taxes or expenses that you have already captured in the Net Worth section. This includes mortgage and other loan payments, insurance premiums, and property taxes and maintenance fees.

There are two options when it comes to inputting living expenses- the quick and easy Simple Approach, and a more granular Detailed Worksheet:

The Simple Approach will ask you for a single amount, representing the sum total of the client's average monthly spending.

The Detailed Worksheet allows you to break out expenses into more specific expense categories, the sum of which will make up a client's monthly living expenses.

When using the Detailed worksheet, the expense categories are shared between the pre-retirement and retirement living expense cards, as well as the Budget module. If you've already filled out a detailed expense worksheet in either of these other locations, you can choose to copy the values into the retirement living expense card via the "Copy From" button:

Customze your expense categories!

Budget / expense categories can be customized on a per client basis within the Gear Icon > Settings > Budget Categories tab. This can only be done after completing the initial data entry process.

To learn more about custom expense categories in RightCapital, click here.

Retirement Living Expenses can be tracked within the projections by navigating to the Cash Flows module in the Retirement section. Within the Cash Flows > Summary, click into the Expenses > Living Expense column:

Like pre-retirement living expenses, retirement expenses will increase based on your general inflation rate by default. However, the retirement expense card provides the flexibility to utilize a number of retirement spending strategies, in addition to the default 'Inflation Adjusted' strategy:

RightCapital provides four additional dynamic spending strategies, incorporating behavioral conditions and market performance when projecting expenses into the future. You can even create your own custom retirement spending strategies within the Models > Retirement Spending tab of the Advisor Portal.

Learn more about Retirement Spending Strategies...

To learn more about creating and implementing retirement spending strategies in RightCapital, please feel free to utilize the resources below:

The Retirement Health Care Cost goal card allows you to reflect a client's expected healthcare costs in retirement:

The Goal starts input determines when the health care costs will kick in for each client, and the Cost estimate controls how the costs are calculated. By default this card will reflect a national average, but costs can be fully customized. There's also a detailed estimate which will allow RightCapital to calculate healthcare costs based on AGI. Retirement healthcare costs will increase based on your health care cost inflation rate.

For more details, please click the link below for our dedicated article on Retirement Health Care Costs:

The fourth and final prepopulated card is the Retirement LTC Cost card, which allows you to input expected LTC costs into your client plans:

By default, LTC costs will be set to the national average for in-home care, and will occur in the last two years of each client's plan. Just like healthcare costs, you can fully customize the timing and cost of long-term care expenses in RightCapital. LTC costs will increase based on your health care cost inflation rate.

Please click on the dropdowns below for more information on...

RightCapital allows you to choose between a number of national averages for LTC, including in-home care, assisted living, and nursing home care. You can also choose the 'customized amount' option to enter your own annual dollar amount for one or both clients.

We review and update these averages on an annual basis.

LTC expenses can occur anywhere from 1 to 10 years from the end of each client's plan. A client's end of plan is determined by the 'Planning Horizon' input, which is entered into the Client and Co-client cards within the Profile > Family section.

To remove long term care costs for a client, you can select the 'No long term care' option within the LTC duration dropdown.

By checking the box beneath the Cost estimate, you can choose to have Retirement Living Expenses stop when the last LTC event begins within the retirement projections.

LTC costs will increase each year based on your Health Care Inflation Rate, and can be tracked within the projections by navigating to the Cash Flows module in the Retirement section. Within the Cash Flows > Summary, click into the Expenses > Health Care column:

From a tax perspective, LTC costs are treated as itemized deductions, and will typically reduce federal tax payments within the cash flows. You can find LTC costs on the sample tax forms in the Tax > Tax Estimate > Details tab, on Line 1 of the Schedule A, and Line 12a of the 1040.

To add additional goals to a client plan, click the blue 'Add Goal' button in the upper right. This will allow you to choose from a long list of options:

Below you will find a brief overview of each goal card, along with data entry details and additional information. Remember that if you ever have any questions while entering client data, you can always reach out to the RightCapital Support Team for assistance!

Pre-College and College goals can both be added to financial plans by clicking Add Goal > Education. If one or more children are added to the Family Profile, RightCapital will automatically generate a College goal for each child within the Goals area.

All amounts are expressed in current dollars, and are inflated within the projections using your Education inflation rate. Both pre-college and college goals will be pulled into RightCapital's Education module, allowing you to curate education funding proposals for your clients.

Please click on the dropdowns below for more information on...

Student: Choose an individual within the plan as the student. This can be the client or co-client, children, grandchildren, or other family members.

Goal starts & Goal ends: Specify the duration of the college goal. By default, this will be set to the student's age 18 to age 21.

College: Determine the cost of the college goal by choosing one of the following options.

National average:Lets you choose between a number of national averages using the dropdown menu to the right. National average costs are from CollegeBoard.org published data, and are updated on an annual basis.

Specific college: Lets you use the College Lookup tool to search for a specific school, automatically pulling in up-to-date tuition costs. Specific college costs are taken from published Department of Education data, and are updated on an annual basis.

Customized amount: Lets you enter a customized gross amount.

Scholarship/Grant: Enter any expected annual scholarships or grants, which will reduce the net amount.

Student borrowing: Enter any expected student borrowing, which will reduce the net amount.

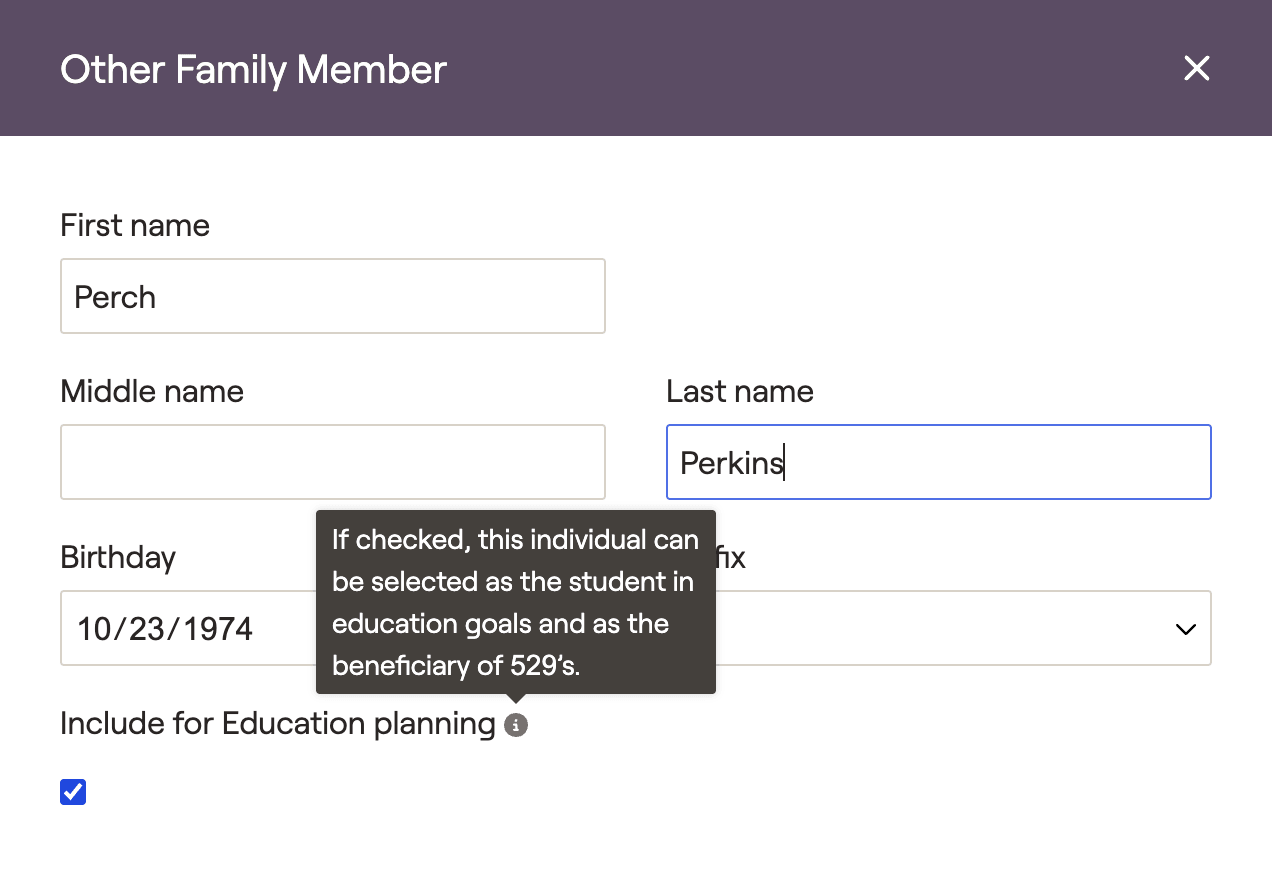

Note on Other Family Members

To select Other Family Members as the student for education goals, navigate to the Profile > Family tab (or Step 1 of the initial six steps of data entry). Open the 'Other Family Member' card, and check the "Include for Education planning" box:

Student: Choose an individual within the plan as the student. This can be the client or co-client, children, grandchildren, or other family members.

Goal starts & Goal ends: Specify the duration of the pre-college goal using calendar years or the age of the student.

Tuition cost: Enter the gross annual amount of the pre-college tuition.

Scholarship/Grant: Enter any expected annual scholarships or grants, which will reduce the net amount.

Student borrowing: Enter any expected student borrowing, which will reduce the net amount.

Note on Pre-College funding

When using 529 accounts to fund pre-college goals, pleasenote that the annual distributions will be capped at $10,000 per the SECURE Act.

Car goals can be utilized to model clients purchasing, leasing, or financing cars within the future projections.

Using the Frequency field, you can specify whether this is a One Time or Recurring Goal. Recurring goals will end once the date specified in the Goal ends field is reached. Choosing the Lease or Finance options within the Buy or lease menu will populate additional fields for the Down Payment, Term, and Interest Rate. A payment schedule will be automatically calculated based on these inputs.

Vacation goals can be utilized to model clients traveling and taking vacations within the future projections.

Modeling vacation goals is quick and straightforward. Enter the Annual amount, choose a Goal starts date, and determine the Frequency of the goal (ex: one-time, every 3 years, etc). If the goal is recurring, choose a Goal ends date as well.

Wedding goals can be utilized to model clients paying for weddings within the future projections. Within the wedding card, you will specify the cost and anticipated year of the wedding.

Asset purchase goals allow you to model the future purchase of lifestyle and business assets within a plan. Both can be added by clicking Add Goal > Asset Purchase.

In addition to the Owner, Purchase price, and Year of Purchase, you'll also have full control over any Annual appreciation. If the client is purchasing the asset up front, you can enter a Down payment of 100%. If not, you can specify the Loan rate and Term to allow RightCapital to calculate a loan balance and payment schedule.

For more information on entering business assets in RightCapital, we recommend reviewing our dedicated article on Business Assets using the link below:

Cash Reserve Goals are only available if you are using the "Use cash reserve goal to manage cash levels" setting for Cash management. This setting can be changed within a client plan by navigating to Gear Icon > Settings > Methodology.

For more information, please click the link below for our dedicated article on the Cash Reserve Goal.

Gift goals allow you to model unique estate & tax planning scenarios by choosing from two gift goal options: Personal Gifts, and Charitable Giving. These goal cards can both be added by clicking Add Goal > Gift.

Personal Gift and Charitable Giving goals will allow for values up to $100,000,000.

Please click on the dropdowns below for more information on...

Personal Gift goal cards allows you to model a gift from the client to another individual. You can specify who the gift is for (which can be a specific child, grandchild, or other family member entered in the Family Profile), or you can select “Other individual” if you don’t want to enter the specific person’s name. Personal gifts can be entered as a percentage of salary income, or an annual dollar amount.

Any gift to a single individual in excess of the annual gift tax exclusion will reduce the client’s lifetime gift/estate tax exemption amount, which could ultimately result in higher estate taxes reflected in the Estate analysis.

Charitable Giving goal cards allow you to model donating assets to a charity or donor advised fund. Charitable giving can be entered as an annual amount or a percentage of salary income.

All asset types can be given to the “Charity” recipient while only cash and appreciated assets can be given to a “Donor Advised Fund”. If charitable giving and other deductions exceed the standard deduction in a given year, RightCapital will automatically itemize deductions when calculating taxes.

When adding a charitable giving goal card, the ‘type’ field allows you to specify the following charitable giving strategies:

Cash: This charitable giving type can be used to reflect a scenario where clients are donating cash to charity or Donor Advised Fund. When donating cash to a donor advised fund the amount is added to the DAF balance listed in the Profile > Net Worth.

Appreciated asset to charity: This can be used to reflect scenarios such as someone donating stock or tangible assets to a charity or Donor Advised Fund. When donating appreciated assets to donor advised fund, the assets will be added to the DAF balance listed in the Profile > Net Worth.

When this option is selected, you can enter a ‘cost basis ratio’ which is the percentage of the amount that is basis, as opposed to growth. When a stock or asset is donated to charity, there are no capital gains taxes paid when assets are liquidated.

For example: if a stock was purchased at $20,000 and is now worth $100,000, the cost basis ratio should be 20%.

Donor Advised Fund: Distributing from donor advised fund to charity will reduce the balance of the DAF listed in the Profile > Net Worth by the amount specified.

Donor Advised Funds

Since funds in a DAF must be used for charitable donations, clients receive a tax deduction for the entire contribution to the DAF in the year it is made, even if the funds are donated to charity in future years.

Investment accounts that are set up as ‘donor advised accounts’ in the Net Worth are not considered part of the client’s invested assets but will still be tracked as part of their net worth.

Donor advised fund balances are tracked in the ‘Other asset’ category on the Net Worth cash flow page.

IRA (Qualified charitable distribution): This allows individuals over 70.5 to donate funds from an IRA directly to a charity tax-free. QCD's will also count towards their required minimum distribution for that year. When selected, you will see a Planned Distribution in the Retirement > Cash Flows as well as a goal to reflect the contribution to charity.

Inherited IRA (Qualified charitable distribution): This allows individuals over 70.5 to donate funds from an Inherited IRA directly to a charity tax-free. QCD's will also count towards their required minimum distribution for that year. When selected, you will see a Planned Distribution in the Retirement > Cash Flows as well as a goal to reflect the contribution to charity.

IRA annuity (Qualified charitable distribution): This allows individuals over 70.5 to donate funds from a qualified annuity to a charity tax-free QCD's will also count towards their required minimum distribution for that year. This is only available if the distribution setting for the annuity is ‘Regular withdrawals’. When selected, you will see a Planned Distribution in the Retirement > Cash Flows as well as a goal to reflect the contribution to charity.

Pro Tip

To offset scheduled RMD's with QCD's in the cash flow projection, select the "Greater of RMD's and Manual Distributions" setting in the Gear Icon > Settings > Methodology tab.

Legacy goals can be utilized to model a specified amount that clients would like to pass to heirs at the end of the plan.

Enter the dollar amount of the legacy goal in the Target amount field, and then choose when the legacy goal will exit the plan as a cash outflow using the Legacy field. Lastly, use the Annual increase to determine which inflation rate will be used to project the target amount out into the future.

If you'd prefer to enter a future dollar amount, you can leave the Annual Increase field set to 'No inflation'.

Other Goal cards can be used as a catch-all to enter any additional goals into a client plan. These cards give you full control over the dollar amount, timing, frequency, and inflation.

A Few Additional Tips:

To set a one-time goal, set the start year and end year to the same client age or calendar year (or set the frequency to “one time”).

To set an annual goal, set the start date to the first year you want the goal to be funded, the end date to the last year you want the goal to be funded, and set the frequency to “Every 1 Year”.