- Income - where the household's primary income sources are entered. This includes client salaries and social security benefits, as well as other income streams such as self-employment income, pension income, and more.

- Savings - where you will enter prospective annual contributions to a client's various investments. This includes contributions to 401(k) and IRAs, taxable brokerage accounts, Roth accounts, 529s, and much more.

- Expenses - where a number of important variables are specified within the plan. This area is where you'll input pre-retirement living expenses, medical expenses, and extra debt payments.

Income

Default Income Cards

There will be a number of income cards pre-populated within this section when you create a new client plan. There will be a Salary card present for each client, as well as a Social Security card:

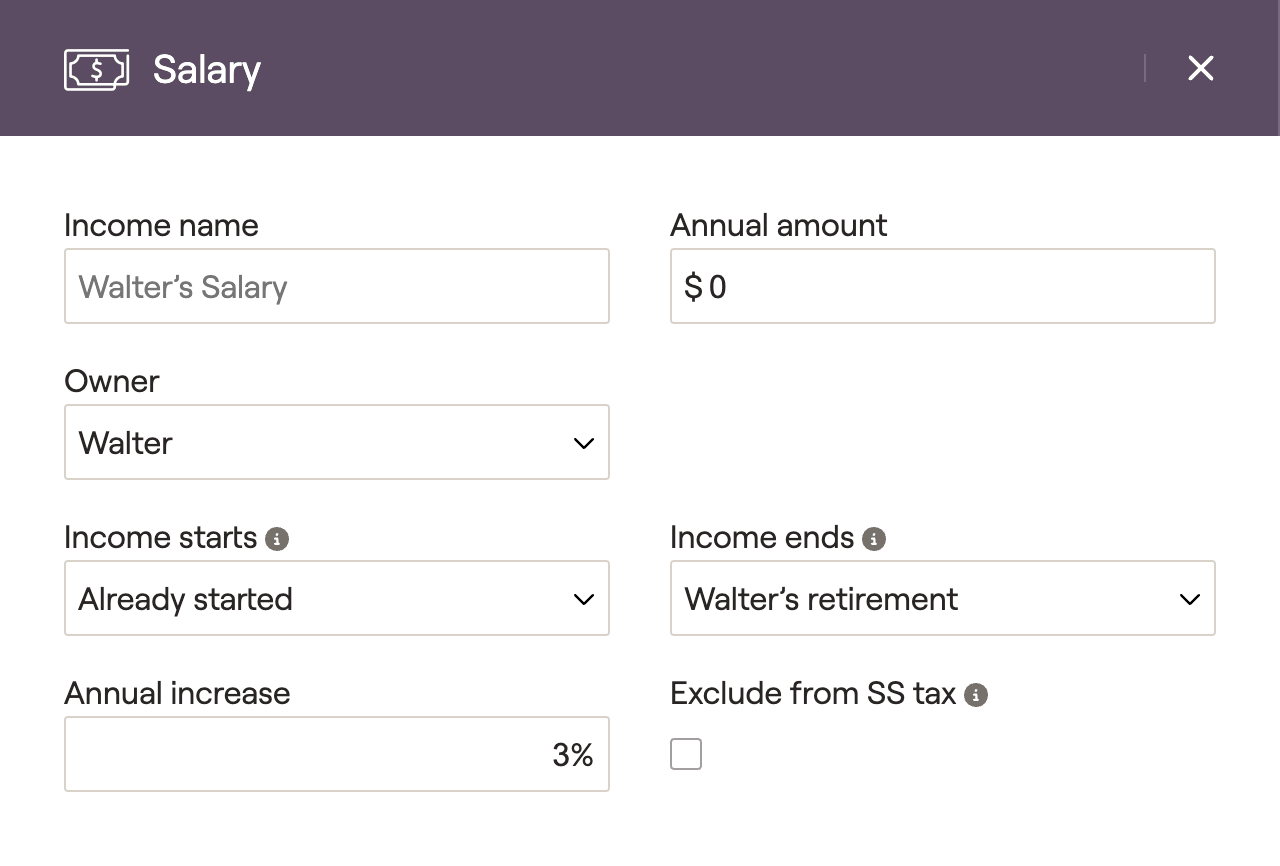

Salary Card

For clients with W2 income, you can utilize the pre-populated Salary cards for one or both clients. Click on this card to open a data entry drawer on the right side of your screen, allowing you to input the salary information:

Please click on the dropdown arrows below for more information on...

Social Security Card

The other pre-populated entry within the Income section is the Social Security card. This card can be used to reflect both current and future Social Security retirement benefits. Click on this card to open a data entry drawer on the right side of your screen:

- Use Simple Estimate - Benefits are estimated using the annual amount and projected annual increase entered into that client’s Salary or Self-employment income card.

- Based on SS Statement Value - You will be asked to enter the monthly benefit amount and corresponding start age from the client's Social Security statement.

- Based on Historical Covered Earning - You will be asked to enter the client's annual covered earnings history.

- No Social Security - RightCapital will not calculate a retirement benefit for the client. We will also exclude any spousal or survivor benefits for that individual.

For a more detailed walkthrough of the data entry process for Social Security, please feel free to reference the article below:

Please click on the dropdown arrows below for more information on...

Add Income

To add additional sources of income to a client plan, click the blue 'Add' button in the upper right. This will allow you to choose from a long list of income options:

For more information on self-employment income, pension income, and other types of income in RightCapital, feel free to visit the link below:

Savings

Default Savings Cards

There will be a handful of savings cards pre-populated within this section when you create a new client plan. You will always find one 401(k) savings card for each client. You may also see a Taxable savings card, depending on your plan settings.

401(k) Savings Card

For clients with 401(k) accounts, you can use the pre-populated 401(k) savings cards for one or both clients. Click on this card to open a data entry drawer on the right side of your screen, allowing you to input the details:

A common example might look like a full match of 100% up to 3% of the client's contribution, and a partial match of 50% up to 5% of the client's contribution:

Please click on the dropdown arrows below for more information on...

Taxable Savings Card

If your Planning Method setting is set to 'Modified Cash Flow Based' or 'Goal Based' as a default, a Taxable savings card will also be pre-populated in the Savings area. Use this card to reflect after-tax contributions into a taxable investment / brokerage account:

If you are using a 'Cash Flow Based' planning method, any and all excess cash flows will be automatically saved and reinvested into the client's taxable account bucket. This function eliminates the need for you to manually enter taxable savings.

To learn more about the planning method setting and its impact on your client plans, feel free to reference the article below:

Please note that taxable savings will only occur in years that clients have adequate income to make those savings. For example, if you enter $10,000 in taxable savings and the clients only have a $5,000 cash flow surplus in a given year, only $5,000 will be saved. In years with cash flow deficits, taxable savings will not occur.

Add Savings

To add additional savings to a client plan, click the blue 'Add' button in the upper right. This will allow you to choose from a long list of savings options:

For more information on 403(b)/457(b) savings, Traditional and Roth IRA savings, and other types of income in RightCapital, feel free to visit the link below:

Expenses

Default Expense Cards

There will be one expense card pre-populated within this section when you create a new client plan: the Pre-retirement Living Expenses card:

Pre-retirement Living Expenses

For clients that have yet to retire, the pre-retirement living expenses card can be utilized to capture the household's monthly expenses within the projections. Click on this card to open a data entry drawer on the right side of your screen, allowing you to input the expense information.

- The Simple Approach will ask you for a single amount, representing the sum total of the client's average monthly spending.

- The Detailed Worksheet allows you to break out expenses into more specific expense categories, the sum of which will make up a client's monthly living expenses.

To learn more about custom expense categories in RightCapital, click here.

Add Expenses

To add additional expenses to a client plan, click the blue 'Add' button in the upper right. This will allow you to choose from the following options:

For more information on medical expenses, extra debt payments, and other expenses in RightCapital, feel free to visit the link below: