Explore Debt Management in RightCapital

Debt Overview

RightCapital's dedicated debt management tool allows advisors to easily demonstrate the value of eliminating debt in a financial plan using specific debt reduction strategies. Before implementing these strategies advisors can view all the necessary information regarding account balances, minimum payments, and annual percentage rate (APR). This allows the adviser to view all debts in one location and determine the best approach for each client's needs:

The Debt module is made up of three subtabs: Strategy, Payment, and Details:

- The Strategy Tab is where you can curate a Proposed Payment Strategy for a client, and compare your strategy to the client's current debt payment strategy.

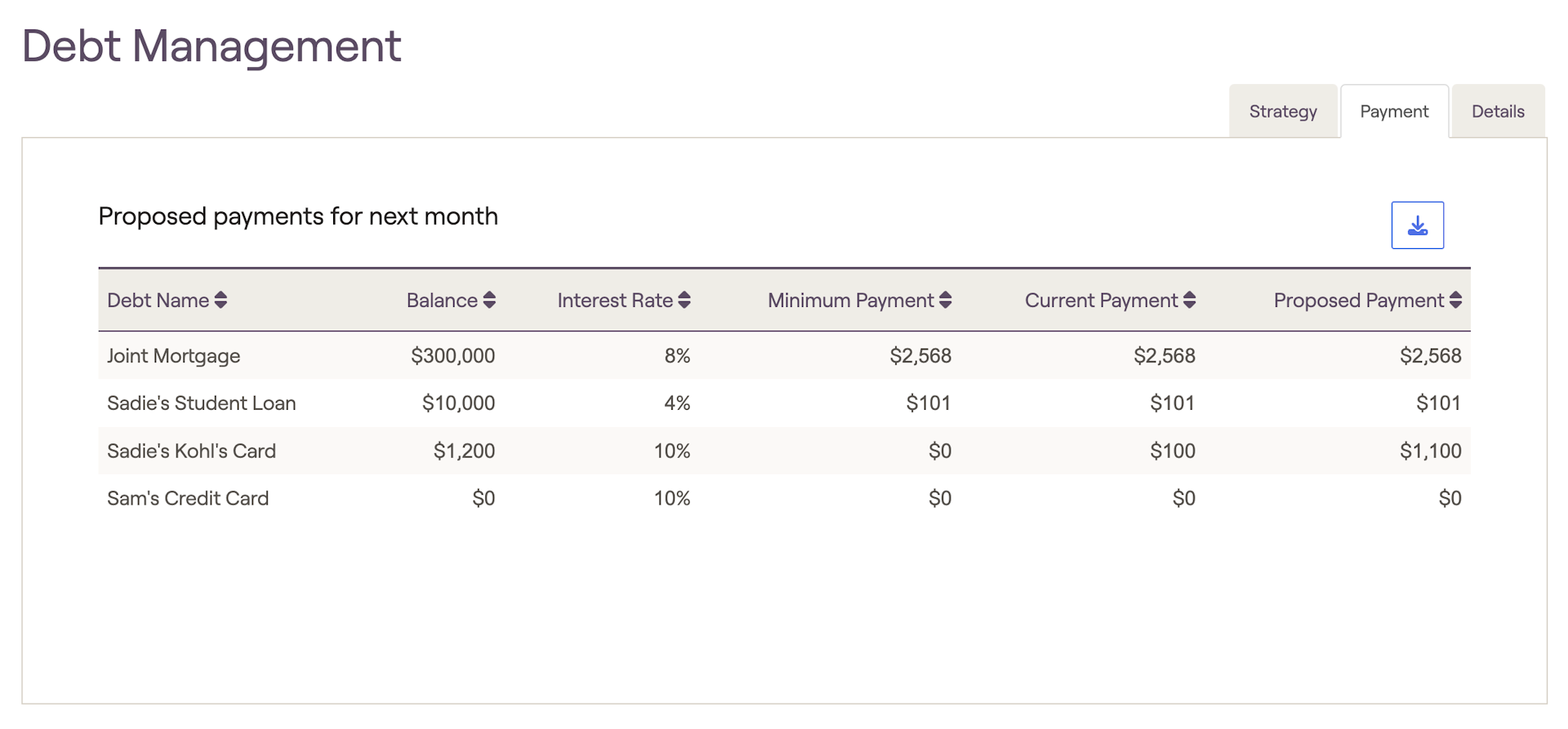

- The Payment Tab is where you can find a breakdown of each loan in the plan, providing you crucial details on their current loans.

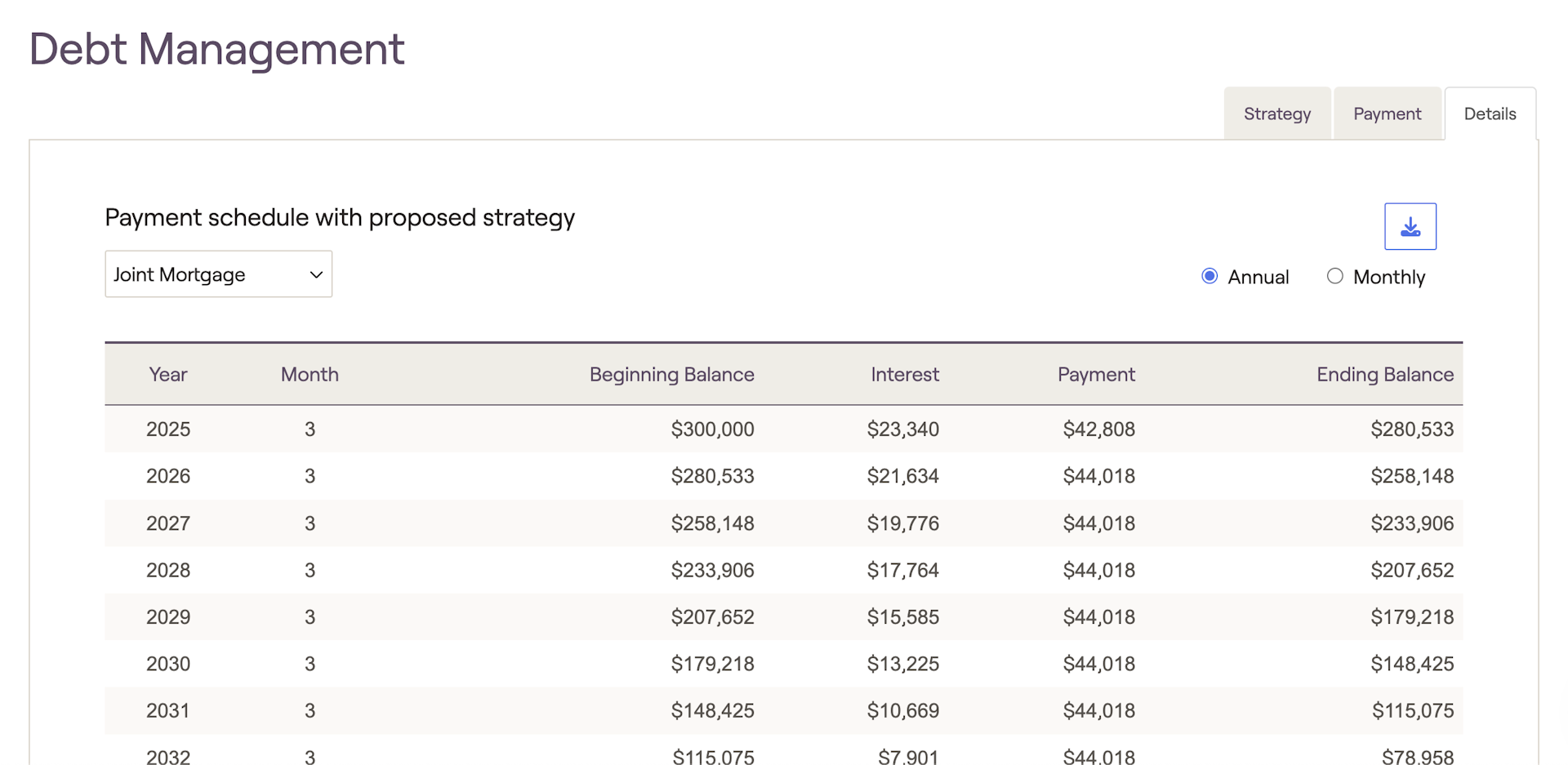

- The Details Tab allows you to view the amortization schedules for each loan in the Proposed Payment Strategy on an annual or monthly basis.

Strategy Tab

Individual debt strategy

Choose which loans you would like to include in your proposed payment strategy within the Individual Loan Strategy section of the Action Items. To exclude a particular loan from the proposed payment strategy, switch to "Keep Current Payments" within the Strategy column for that loan:

Under the Strategy menu, you will find additional options to model alternative payment strategies.

- Prioritize Highest Rate: Prioritizing debt payments from the highest to the lowest interest rate is known as the "debt avalanche" strategy. This saves money on interest payments by quickly paying down the principal balance on high-interest debt. This method reduces the interest accruing on debts which can heavily impact total costs.

- Prioritize Balance: Prioritizing debt payments from lowest to highest balance is known as the "debt snowball strategy". This strategy allows clients to gain momentum by paying off multiple debts in a short period of time. Although this strategy saves less on interest when compared to the "debt avalanche" method, it can offer encouragement for clients who are overwhelmed with multiple debt payments.

In each strategy, the minimum payments are met but the total monthly debt payments do not decrease as the debt is paid off. Instead, as each liability is eliminated, the previous payment gets rolled into the next prioritized debt. Additionally, you have the option to shift available cash flow towards the prioritized debt as additional payments.

Borrowers can seek to refinance their debt in order to make favorable changes in their credit agreements. In this scenario, the original contract is replaced with new terms that offer updated payment schedules, lower interest rates, and reduced monthly payments. Typically borrowers will refinance mortgages, car loans, or student loans as interest rates fall in response to changing economic conditions.

Extra Debt Payments

Within the debt module, you are able to model extra debt payments towards specific loans on a singular or reoccurring basis, as opposed to increasing the existing monthly payment.

This option will allow you to specify the extra debt payment amount, loan, frequency, and date. Press "save" to add the debt payment to the plan.

Once saved, the extra debt payment will then be displayed in the action items. The extra debt payment details can be adjusted by selecting the frequency option, or by adjusting the payment slider.

To remove an extra debt payment from the debt strategy, simply open the edit menu, and deselect the extra debt payment.

Adjusted rate mortgages, Interest only mortgages, Home equity lines of credit, and Reverse mortgages are not included in the proposed payment strategies due to the complex calculations involved.

Payment Tab

Details Tab

Applying Your Debt Proposal in the Retirement Analysis

In the right-hand column under Strategies, find the Debt Strategy item, toggle from "Current Payments" to "Debt Proposal", and click the Refresh button in the lower right. This will cause the proposed payment strategy from the Debt module to be incorporated into your proposed plan:

Interaction with Student Loans

In addition, no changes to the Student Loan planning module will impact what is reflected on the Debt screen or vice versa.