For clients with Traditional IRAs, you can enter ongoing contributions within the Savings section of the Profile (or the Savings step of the initial data entry process). These savings cards can be added by clicking Add Saving in the upper right, and selecting Traditional IRA:

IRA Savings Data Entry

Click on this card to open a data entry drawer on the right side of your screen, allowing you to input the contribution information:

1

The Saving name will default to [Client's] Traditional IRA, but you can enter a custom name if you'd like. In joint plans, you will also want to choose either the client or the co-client as the Owner.

2

Enter the client's annual Contribution to their IRA. Depending on the option you choose in the Target field, this can be an annual dollar amount, a % of the client's income, or the maximum contribution amount.

3

Specify the duration of the contributions using the Saving starts and Saving ends fields. By default, these will be set to 'Already started' and '[Client's] retirement' respectively.

4

When entering an annual dollar amount, you can choose to specify an optional Annual increase in the lower left of the card.

Additional Information

Contribution Limits and Taxation

Contributions are capped at the IRS limit ($7,500 for 2026 + $1,100 catch-up for those 50 and over). This cap includes both Traditional IRA and Roth IRA contributions.

For Traditional IRAs, contributions less than the income limit will be considered tax deductible (Line 20 of the Schedule 1, Line 10 of the Sample 1040 Tax Form). In 2026, deductibility phases out between $81,000 and $91,000 of AGI for single; between $129,000 and $149,000 for joint. Over those thresholds, the total contribution will be considered nondeductible.

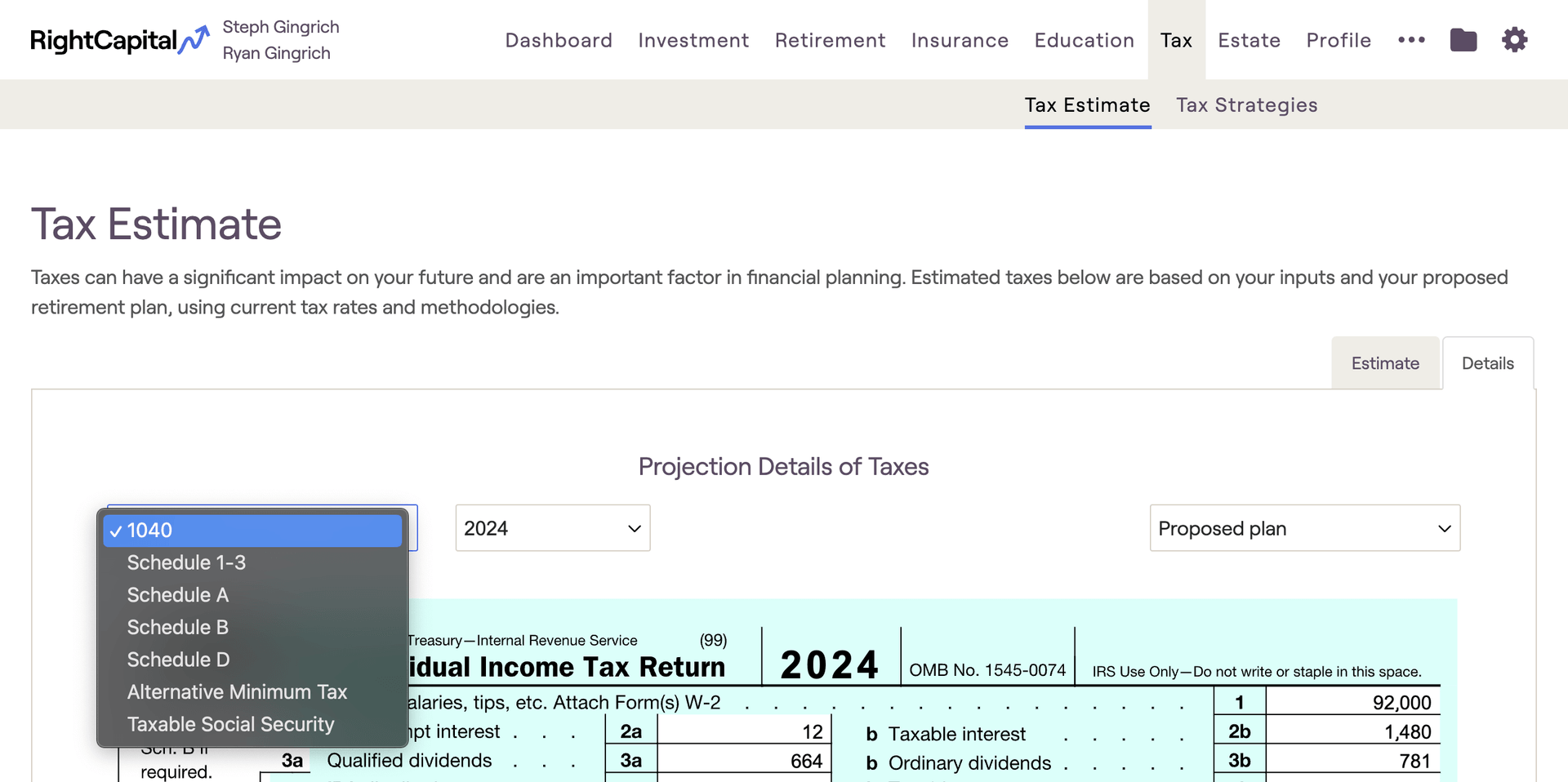

Sample tax forms can be viewed in the Tax > Tax Estimate > Details tab:

Cash Flow Location & Details

Client contributions can be tracked in two locations within the Retirement > Cash Flows:

- The Summary tab > Planned Savings column

- The Invested Asset tab > Planned Savings column

By default, IRA and Roth IRA contributions will be funded using taxable assets in years with cash flow deficits. If the "Use taxable account to fund IRA and 529 saving when current year cash flow is inadequate" setting is unchecked, IRA contributions will not occur in years with inadequate cash flows. You can find this setting in the Gear Icon > Settings > Methodology tab of each client plan: