Illustrate Tax-Efficient Distributions with Ease

Visualize tax impacts overtime on a client's plan

Illustrate the impact of tax-efficient distribution strategies in retirement

Demonstrate how your proposal will save the client from paying higher taxes

Changes made on the Tax Distribution screen will not automatically reflect within the Cash Flow or Tax Estimate projections.

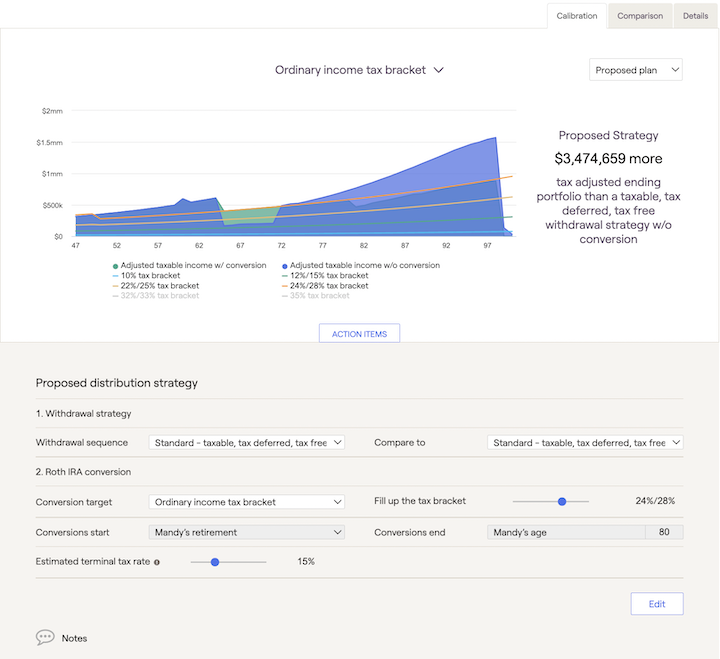

Calibration Tab

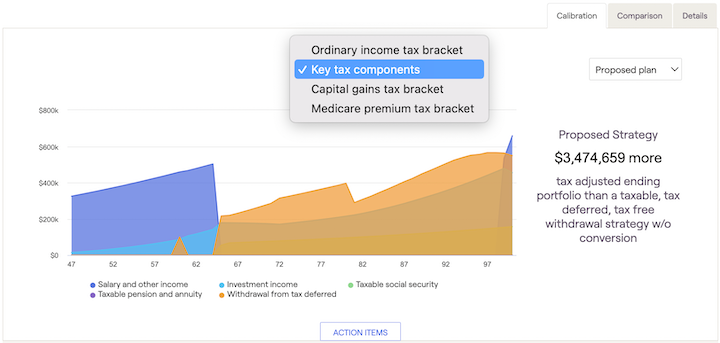

The calibration screen allows advisors to see how close their clients are to income limits for federal income tax brackets, capital gains brackets, and Medicare adjustments. Advisors can also see the key tax components that make up the taxable income during each year of the financial plan. Users can toggle between the different graphs using the dropdown menu above the graph.

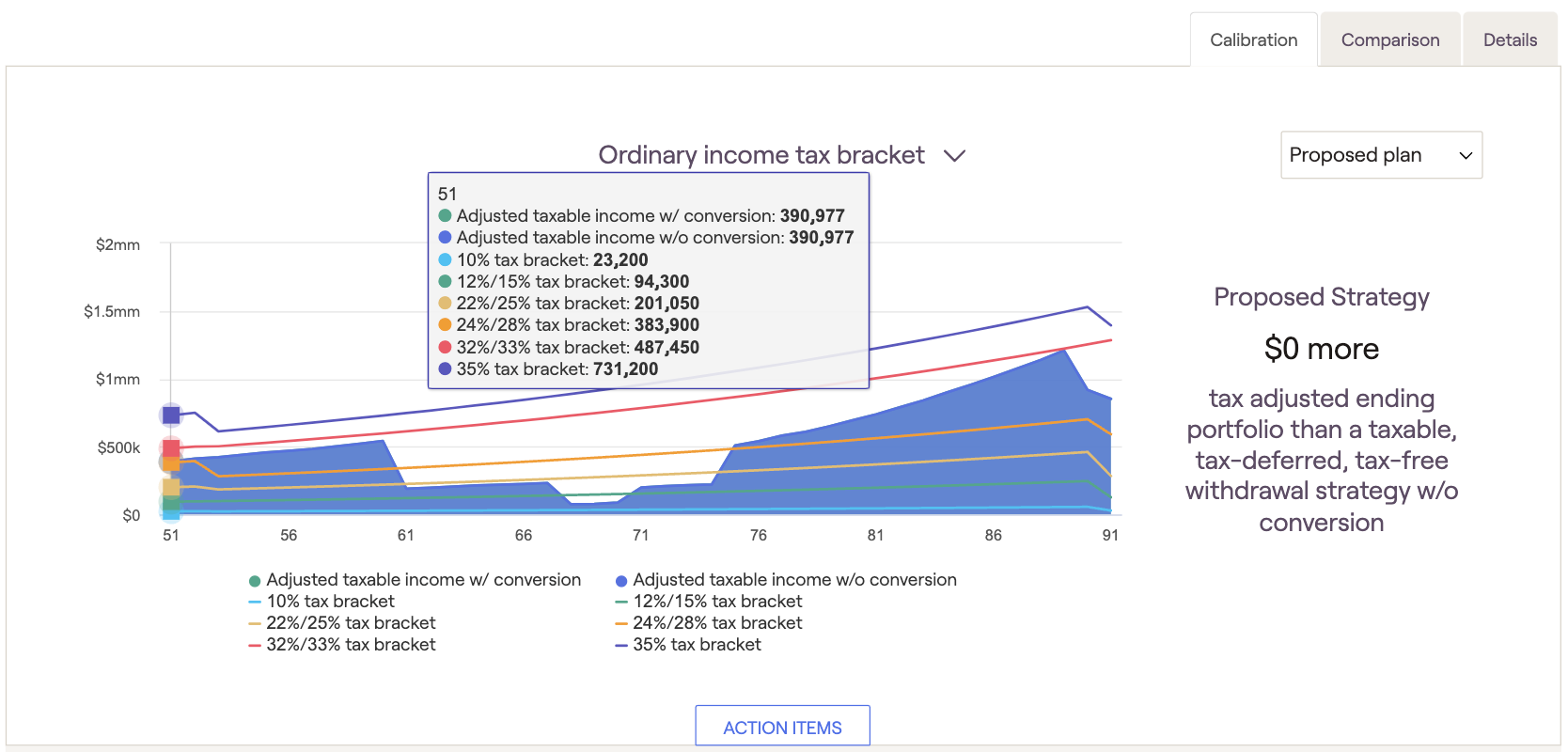

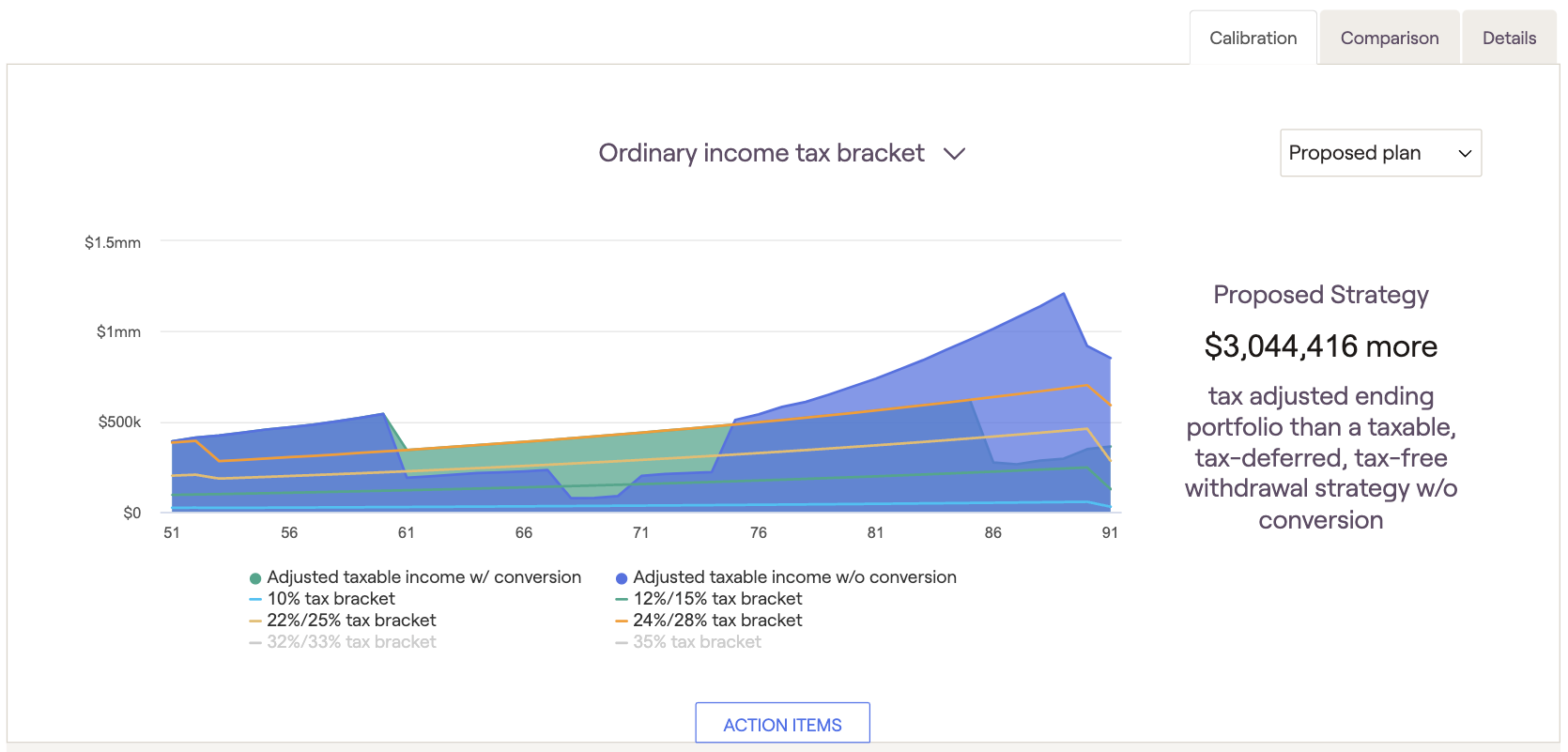

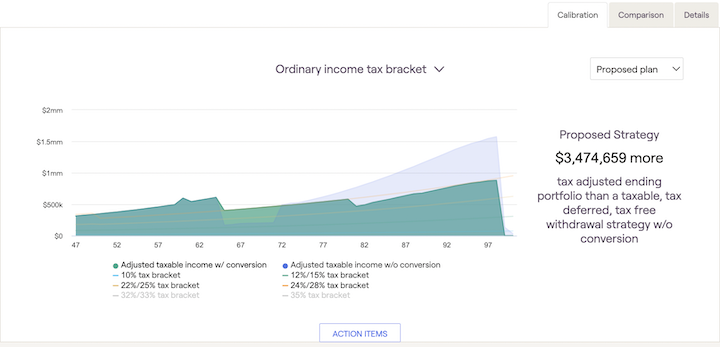

Ordinary income tax bracket graph

The initial chart displayed illustrates the client's adjusted taxable income over time (this is the value used to determine which tax bracket(s) the client falls into) and shows how that compares to different tax brackets over time. It shows how taxable income changes over the course of the projections.

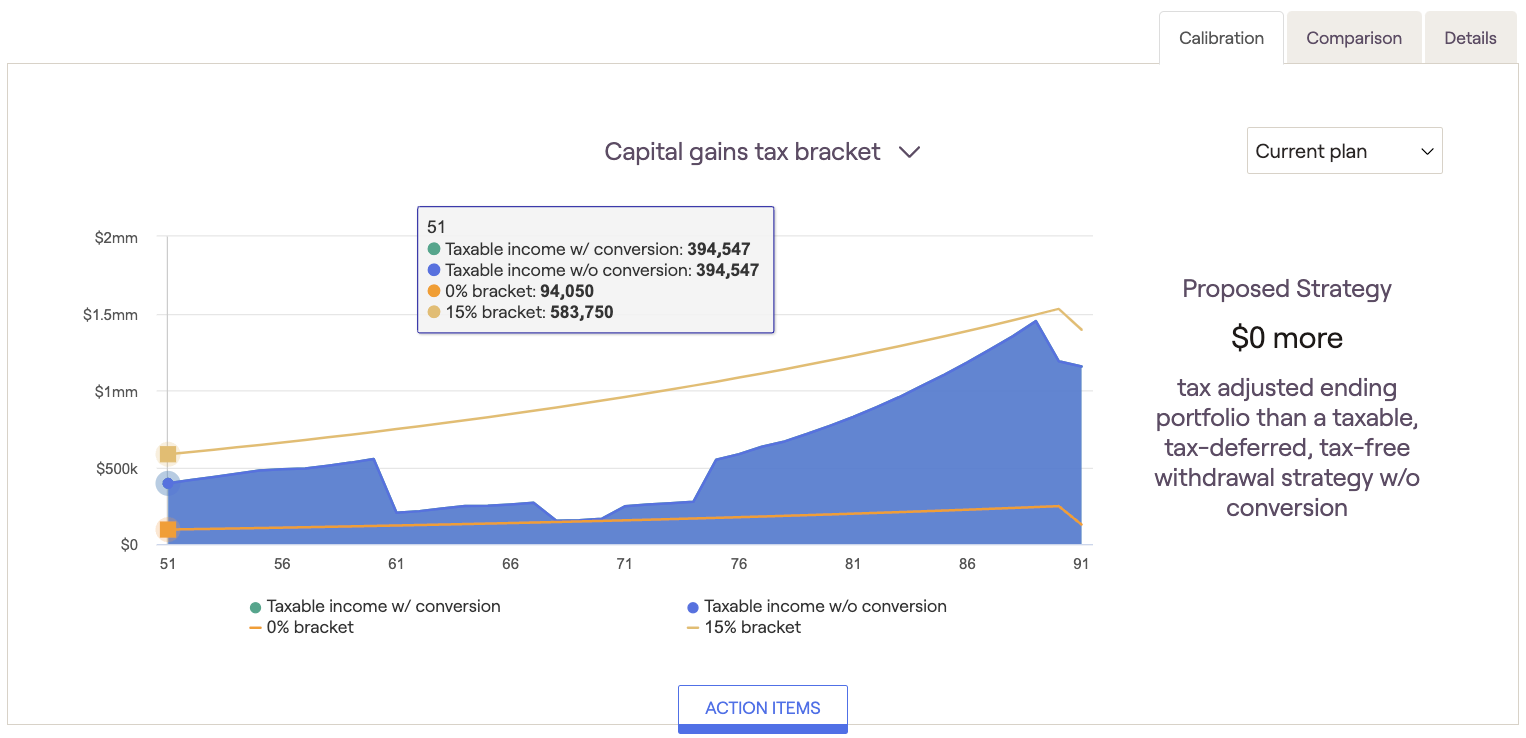

Capital gains tax bracket graph

The capital gains tax bracket graph shows the household’s total taxable income in relation to capital gains tax brackets (0% and 15%). Capital gains income above the 15% bracket will be taxed at 20%.

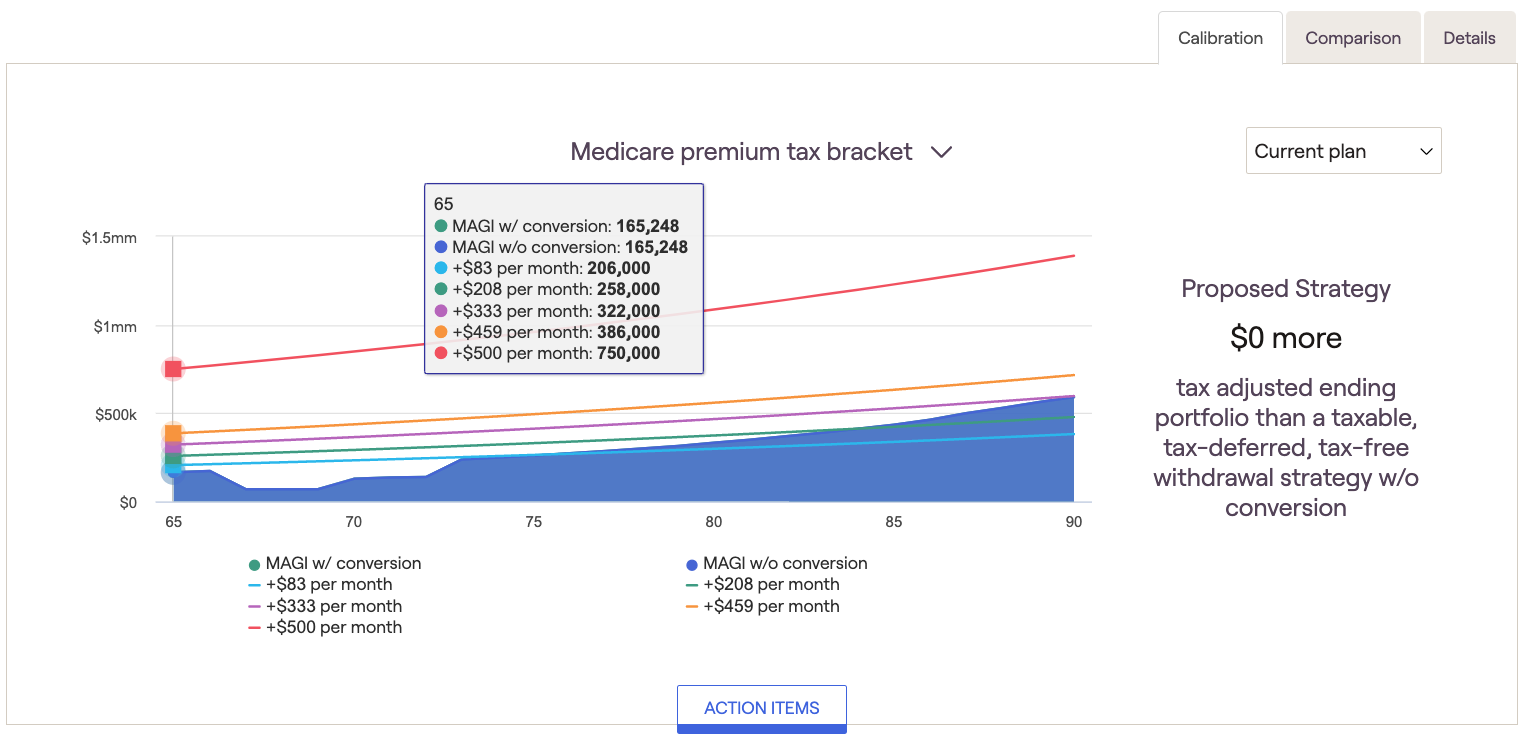

Medicare premium tax bracket graph

The Medicare premium tax bracket graph shows the household’s Modified Adjusted Gross Income (MAGI) used to calculate adjustments to Medicare premiums in relation to the thresholds that trigger higher premiums (IRMAA). The lines on the graph denote the monthly increase in the premium amount based on MAGI thresholds.

Withdrawal Strategy

When funding cash flow needs, RightCapital will default to taking money from taxable accounts first, then tax-deferred accounts, and lastly tax-free accounts. The withdrawal strategy dropdown menu allows users to adjust this distribution sequence and determine the impact on a financial plan.

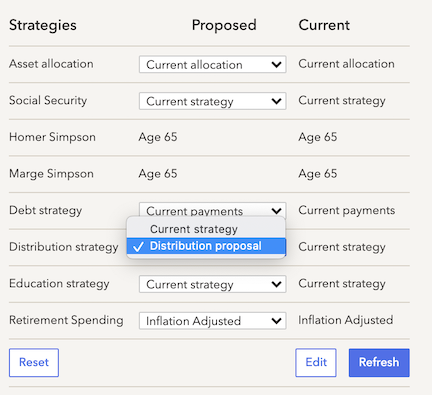

The “compare to” field allows users to adjust the distribution strategy used in the calibration graph comparison. This will impact the value listed on the right side of the calibration graph above. The system defaults to comparing the proposed strategy with Roth Conversions" to a Pro-Rata withdrawal strategy without conversion. If users want to change the withdrawal strategy in a proposed plan they can choose the 'Distribution proposal' in the Retirement > Analysis > Action Items.

If users change the withdrawal sequence to pull funding from 'Tax-deferred, taxable, tax-free', while the client is under 59.5 years old, RightCapital will pull from the taxable account before tax-deferred in the cash flow projections for the proposed plan.

Roth conversions

Additionally, illustrate the impact of Roth conversions on the financial plan. Users can choose a conversion target, then ‘fill up’ specific tax brackets with Roth conversions. Conversions can be used to fill up to ordinary income tax brackets, and capital gains tax brackets, or to illustrate conversions to the point where income-based (‘IRMAA’) adjustments to Medicare premiums would be required.

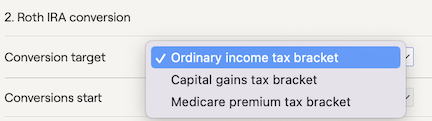

Conversion target

The conversion target will allow users to choose from three separate conversion scenarios:

- If the Ordinary income tax bracket is selected, the user will be able to use the slider bar to select which tax bracket to fill with Roth conversions.

- If the Capital gains tax bracket is selected, there will be a different slider bar that allows the user to fill up to the 0% or 15% capital gains tax brackets, meaning that we will convert as much as possible without exceeding the specified bracket.

- If No IRMAA is selected, RightCapital will convert as much as possible without triggering IRMAA adjustments to Medicare premiums.

After selecting the ordinary income tax bracket or capital gains tax bracket, use the slider in the action items to specify which bracket to fill with Roth Conversions. RightCapital will then calculate the amount that would need to be converted to bring the client's income to the tax bracket specified. The conversions will be generated in any year between the current year and the end of the plan where the adjusted taxable income is less than the specified bracket. Conversion opportunities will show until there are no tax-deferred assets left to convert.

The green-shaded area represents the new pattern of taxable income following the conversion. The conversions bring the taxable income up to the specified tax bracket line.

Conversion Start & End Date

To select the start and end date during which you are proposing Roth Conversions, click the Edit button in the lower right corner of the Action Items. This will allow you to target specific timelines for conversions within the proposed tax-efficient distribution strategy. Start/End dates can be a life event, calendar year, or the client/co-client's age:

Click on items in the legend to turn them on or off in the chart to better show the taxable income with and without conversion.

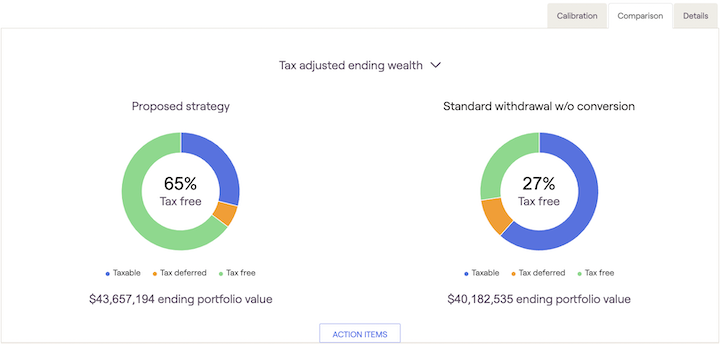

Comparison Tab

Use the drop-down menu to gain deeper insights into the comparison. You can compare withdrawals with a Roth conversion compared to withdrawals without a Roth conversion. There are also options to compare the total account balances, the total Federal tax paid, and the total Required Minimum Distributions, with and without conversions.

Notice that hovering over various elements of the charts and graphs reveals detailed information.

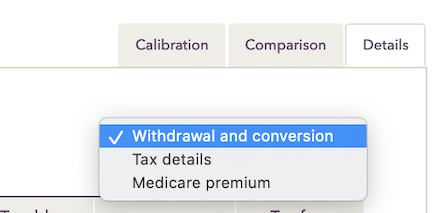

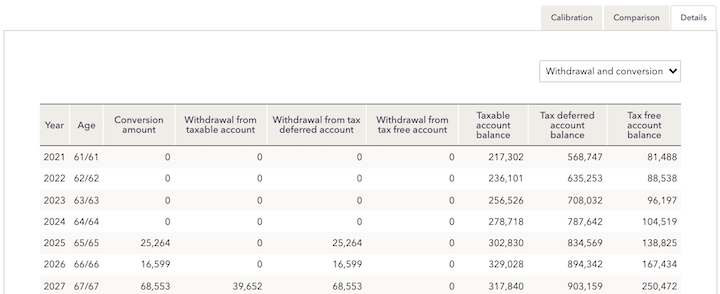

Details Tab

- Withdrawal and conversion will illustrate the amounts generated as converted for each year, as well as other taxable, tax-deferred, and tax-free account data. This cash flow chart will illustrate how much can be converted to Roth each year based on the strategy set within the Calibration & Comparison tab action items. The remaining columns that show "withdrawal from" and "account balance" will emphasize the impact of Roth Conversion and additional taxation on each bucket of assets. It is common to see additional income from accounts needed in years when Roth Conversions are created to fund the additional tax liability.

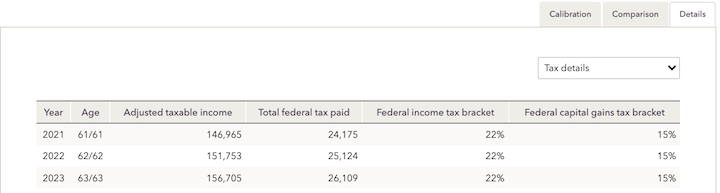

- Tax details show the total federal taxes paid in each year and show the maximum ordinary income and capital gains tax brackets in those years.

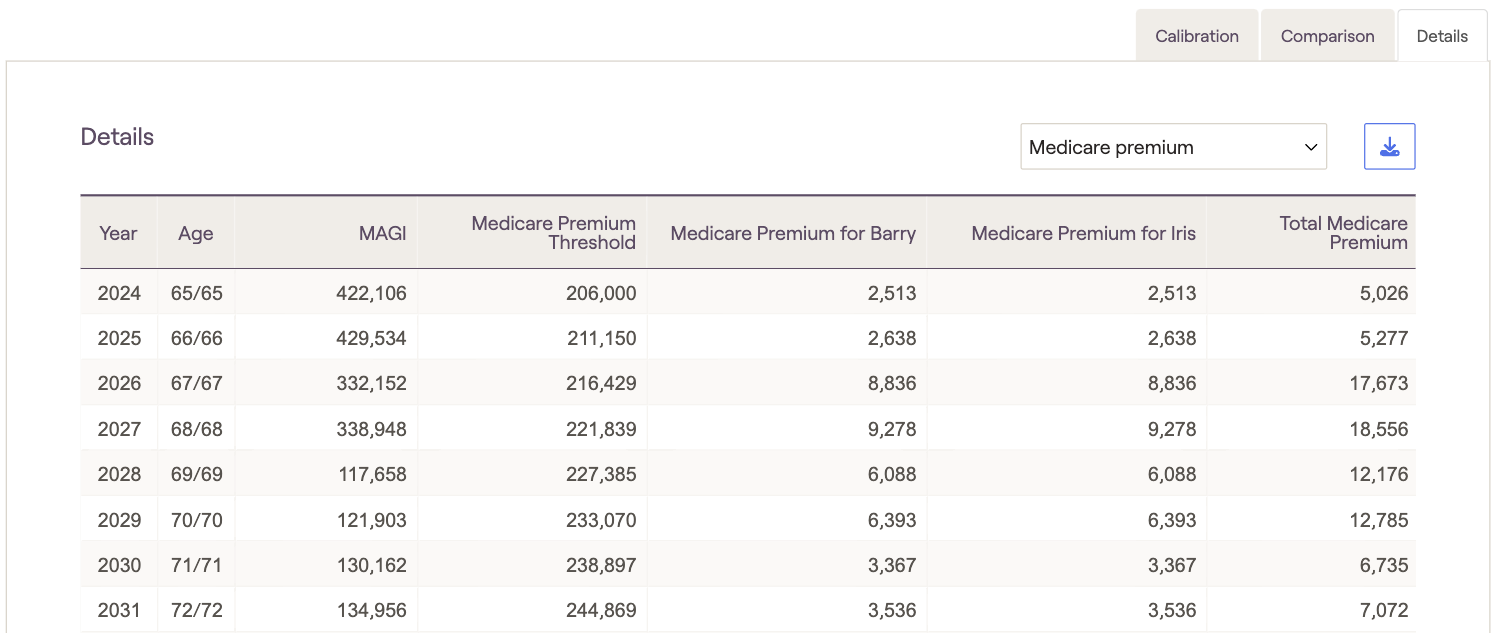

- Medicare premiums show the total Medicare premiums in each year if either client has elected to use the ‘Detailed estimate’ option for Retirement Health Care costs.

Additional impacts: tax brackets and tax law

If the tax law is set to TCJA with the sunset provision, RightCapital will utilize the current tax brackets through 2025 and then revert to the 2017 tax brackets. This is referenced on the screen by listing the respective tax rates associated with the brackets; e.g. the '12%/15% tax bracket' illustrates the current 12% bracket through 2025 and then reverts to the prior 15% bracket.

When using Roth conversions to "fill up" the tax bracket, RightCapital will use the same approach - first to calculate the amount needed to fill the current 12% bracket through 2025 and then to fill the old 15% bracket thereafter.

Reflecting conversions in Monte Carlo projections

Changes made in the Tax Distribution screen can be reflected instantly within any proposed plan. To apply a distribution proposal, visit the Retirement Analysis module and access the action items at the bottom of the screen. On the right side of the action items, advisors can choose the Distribution Strategy. Once the selection is changed to "distribution proposal", details from the Tax Distribution screen will flow into the proposed plan.

To illustrate Roth Conversions in the Current plan, enter a Distribution Income card on the Profile > Income screen.

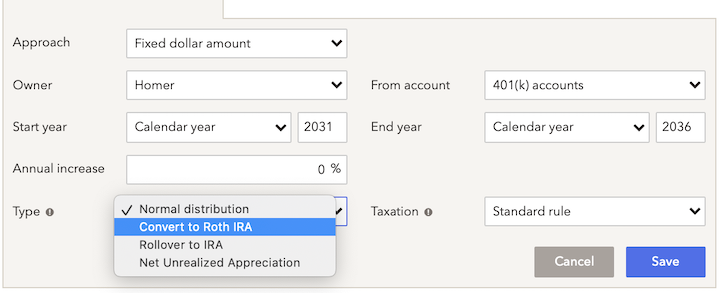

Specify the amount, the year(s) of conversions, and whether they are coming from an IRA or 401(k) account, and select 'Convert to Roth IRA' in the Convert/rollover drop-down box to reflect a Roth conversion.