RightCapital allows advisors to estimate or supply a client’s Social Security retirement benefit within the Profile > Income tab of each financial plan (or Step 2 of the initial data entry). RightCapital will automatically generate a Social Security income card for both the client and co-client within every plan. Click on this card to open it, allowing you to enter that client's current or future benefit:

If the client is already receiving Social Security retirement benefits, check the Already Receiving box in the upper right of the card. You will then be able to enter the monthly amount that they are currently receiving. You will also be asked for the year in which the client began receiving benefits- this allows RightCapital to calculate any spousal benefits for the co-client:

Be sure that social security benefit amounts are entered gross of medicare deductions. Retirement health care costs are reflected as a separate expense in the Profile > Goals tab.

The Filing age and Filing month will determine that client's current strategy for social security. This is when you will see retirement benefits begin in the client's Current Plan within the Retirement > Analysis section. It is also what will be reflected in the Current Strategy for comparison in the Social Security optimization module.

Be aware that Social Security retirement benefits will always begin in the month after filing in the plan. For example, if your selected filing month is January, benefits will not begin until February.

If you choose a specific filing age without specifying a filing month, we assume that Social Security benefits will begin in the month following the client's birthday. Benefits in the first calendar year will be prorated accordingly.

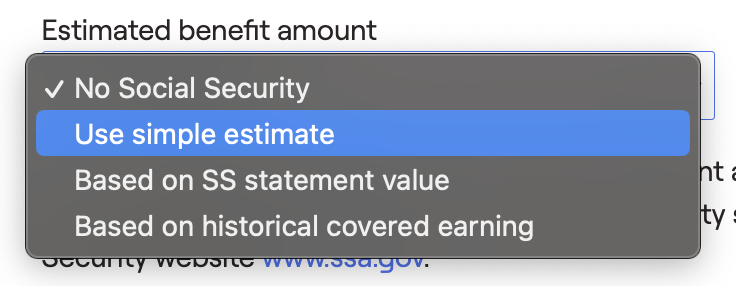

The Estimated benefit amount drop-down box determines how Social Security benefits will be calculated. Each option has different use cases, and will calculate the monthly retirement benefit differently:

‘Use Simple Estimate’ is the default setting in RightCapital. When using this option, no additional inputs are required within this card. The social security benefit is estimated using the income and projected annual increase entered into that client’s Salary or Self-employment income card in the Profile > Income section. The income amount is projected forward and backward to generate a history of earnings, which is then used to determine the benefit amount.

In addition to Salary and Self-employment income cards, the simple estimate will also factor in any Bonus cards entered, as well as Other Income cards that are set to Earned Income.

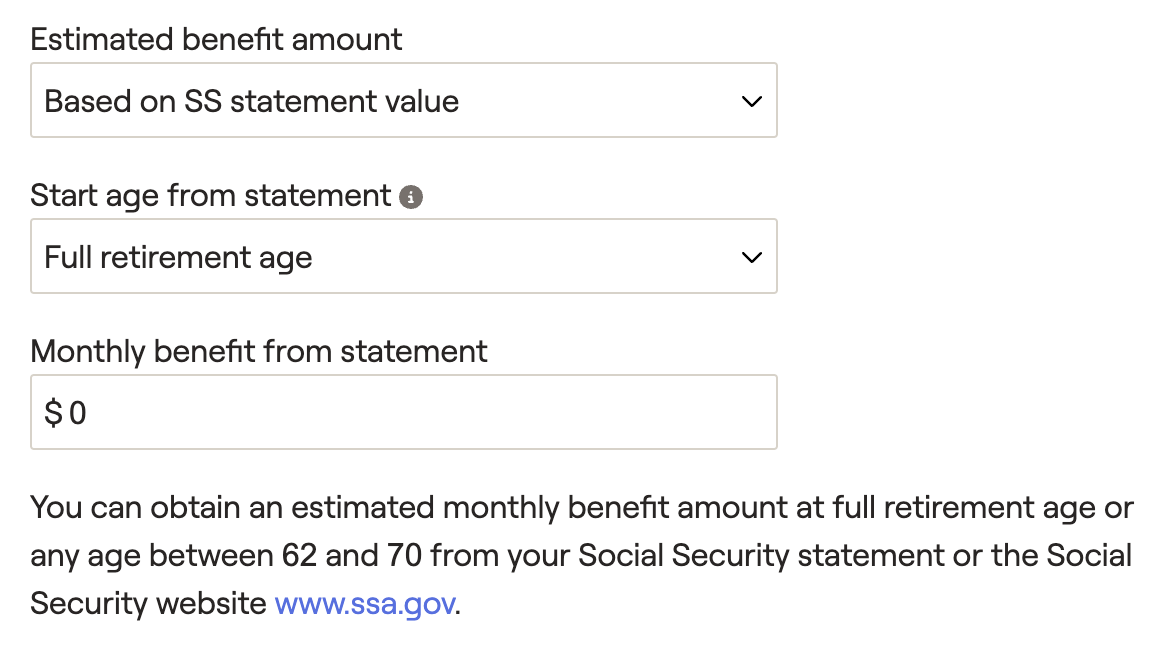

When using the ‘Based on SS Statement Value’ option, you will be prompted to enter the client's projected benefit amount, either at FRA or any other age listed on the client's Social Security statement. RightCapital will reduce benefits or add delay credits to the benefit amount as appropriate based on the filing age selected above. Future income based on a client’s Salary or Self-employment income card will not be factored in when using this option.

Start age from statement: Enter the age that the estimated monthly benefit amount is based on, as seen on the Social Security statement.

Monthly benefit from statement: Enter the estimated monthly benefit amount that corresponds with the start age entered above.

If clients do not have a social security statement, they can receive a benefits estimate via the Social Security website. This link is also included at the bottom of the Social Security income card for your convenience.

"Filing Age" vs. "Start Age from Statement"

When using ‘Based on SS statement value’ as the estimated benefit amount option, the ‘Start age’ is specifically the age listed on the client’s SS statement, along with its corresponding monthly amount. The ‘Filing age’ is when the client is presumed to file in the RightCapital retirement projections. Be mindful not to confuse these two inputs!

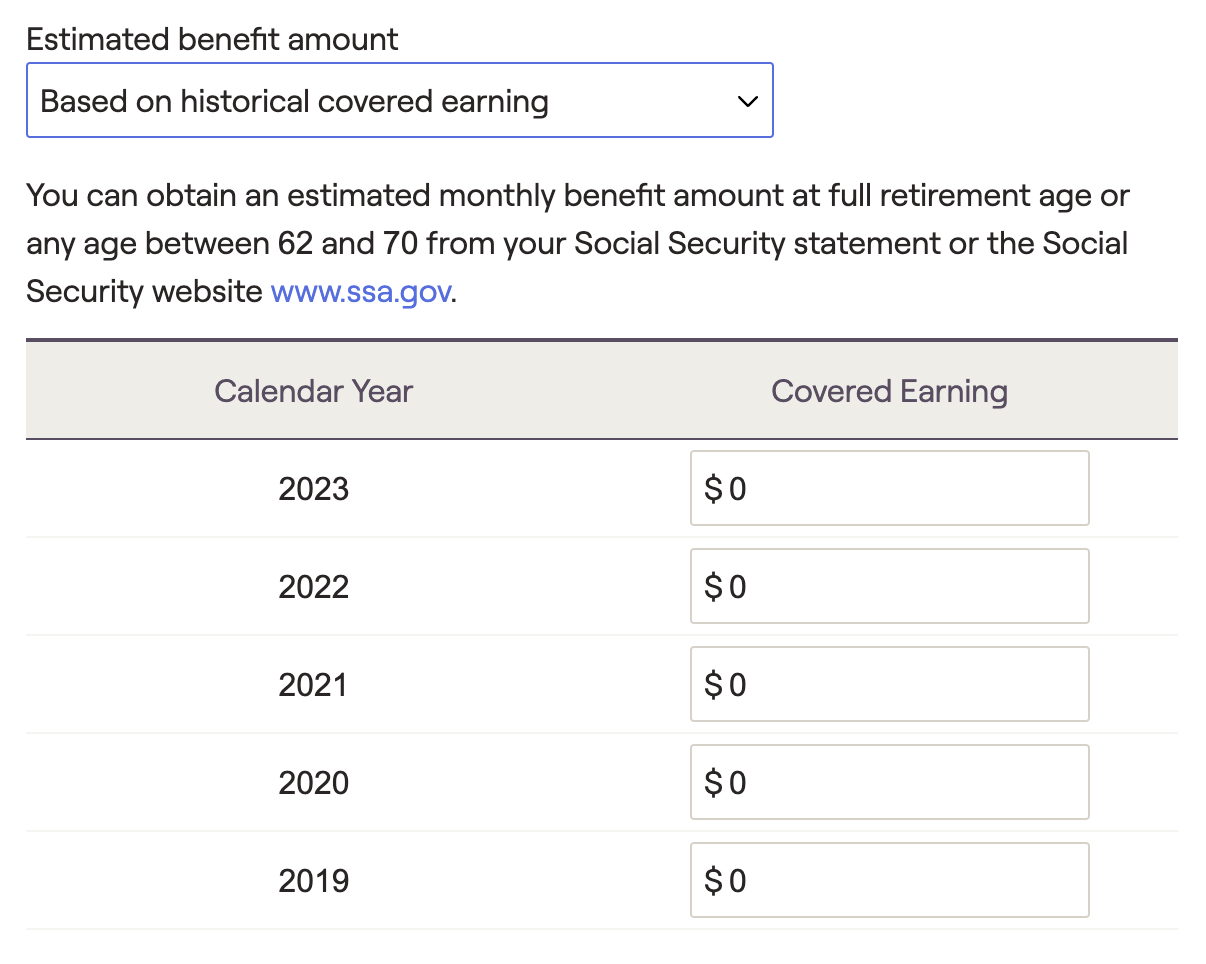

When using the ‘Based on Historical Covered Earning’ option, a detailed worksheet will populate allowing you to enter the client's annual covered earnings history. RightCapital will use those earnings to calculate the client’s Social Security benefit. Future income based on a client’s Salary or Self-employment income card will be factored in when using this option.

Clients can obtain their historical covered earnings from the Social Security website. This link is also included at the bottom of the Social Security income card, for your convenience.

When using the ‘No Social Security’ option, RightCapital will not calculate a retirement benefit for the client. RightCapital will also exclude any spousal or survivor benefits for that individual within the plan.

Although the Social Security income card cannot be deleted, using the ‘No Social Security’ option will functionally turn off this card. Use this option whenever you’d like to prevent or remove a client’s social security benefits in RightCapital.

Social Security Retirement Income can be tracked in the Retirement > Cash Flows > Summary tab. Click into the underlined headers Income Inflows > Social Security for more details:

Spousal benefits do not need to be entered manually within joint plans. RightCapital will automatically generate spousal and survivor benefits when clients are eligible, and financial plans will include the greater of a client's retirement benefit or the spousal/survivor benefit to produce the best outcomes.

To stop RightCapital from automatically including a spousal or survivor benefit, select "No Social Security" as the estimated benefit amount within that client's Social Security income card.

Within single client plans, spousal and survivor benefits based on the record of a divorced or deceased spouse can be entered using a Spouse Social Security card.

Contact Us

For additional assistance within RightCapital please contact our Support team.

Educational Webinars

RightCapital is committed to enabling your success. Each week, we cover essential planning modules and product updates.

RightCapital in Action

Check out our YouTube channel where we highlight Advisor Success Stories and share more Tips & Tricks!